Las Vegas Sands’ Quarterly Earnings Preview: What You Need to Know

/Las%20Vegas%20Sands%20Corp%20phone%20by-%20Piotr%20Swat%20via%20Shutterstock.jpg)

Nevada-based Las Vegas Sands Corp. (LVS) develops, owns, and operates six integrated resorts in Macau and Singapore. Valued at $28 billion by market cap, the company’s integrated resorts feature luxurious accommodations, casinos, entertainment, malls, celebrity chef restaurants, and other amenities.

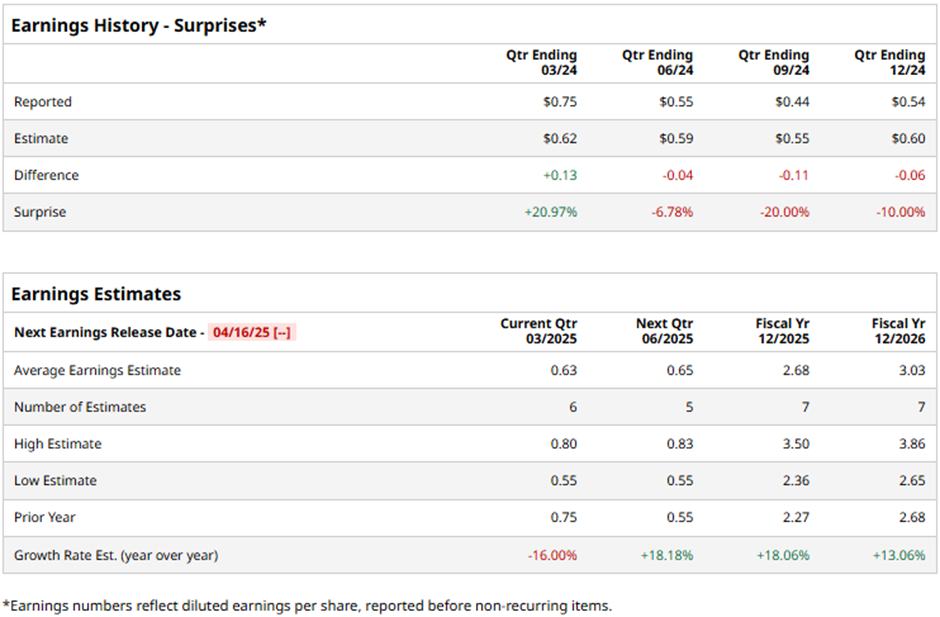

The resort giant is expected to announce its first-quarter results on Wednesday, Apr. 16. Ahead of the event, analysts expect LVS to deliver an adjusted EPS of $0.63, down 16% from $0.75 reported in the year-ago quarter. Meanwhile, the company has a mixed earnings surprise history. It missed the Street’s bottom-line estimates thrice over the past four quarters while exceeding on one other occasion. Its adjusted EPS of $0.54 for the last reported quarter missed the consensus estimates by 10%.

However, for the full fiscal 2025, LVS is expected to report an adjusted EPS of $2.68, up a significant 18.1% from $2.27 in fiscal 2024. Furthermore, its earnings are expected to increase 13.1% year-over-year to $3.03 per share in fiscal 2026.

Over the past 52 weeks, Las Vegas Sands’ stock has tanked 32.5%, significantly underperforming the Consumer Discretionary Select Sector SPDR Fund’s (XLY) 6.2% gains and the S&P 500 Index’s ($SPX) 3.6% uptick during the same time frame.

LVS stock prices soared 11.1% in the trading session after the release of its mixed Q4 results on Jan. 29. Five of the six resorts owned by LVS are located in Macao and the slowdown in the Chinese economy after the COVID-19 pandemic severely impacted the company’s financials. Although spend per visitor has remained below pre-pandemic levels, it has observed some recovery during the quarter. While LVS observed a marginal decline in net revenues compared to the year-ago quarter to $2.9 billion, it surpassed the Street’s expectations by a notable margin which boosted investor confidence.

However, its adjusted net income dropped 10.8% year-over-year to $387 million and missed analysts’ projections. Following the initial surge, LVS stock prices remained in red for five subsequent trading sessions.

Nevertheless, analysts remain optimistic about the stock’s prospects. The consensus opinion on LVS stock is moderately bullish, with an overall “Moderate Buy” rating. Among the 15 analysts covering the stock, 10 recommend “Strong Buy” and five suggest a “Hold” rating. Its mean price target of $57.58 suggests a 58.1% upside potential from current price levels.

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.